Work-related costs scheme: staff allowances

Do you provide staff allowances to your employees? The work-related costs scheme (werkkostenregeling, WKR) allows you to spend part of your total taxable wage (the 'discretionary margin' or 'discretionary scope') without tax liability.

You can use this discretionary margin on:

- reimbursements, for example a reimbursement for a haircut

- benefits in kind, for example Christmas or birthday present

- provisions, for example a company bicycle

Work-related costs scheme: untaxed extras for your staff

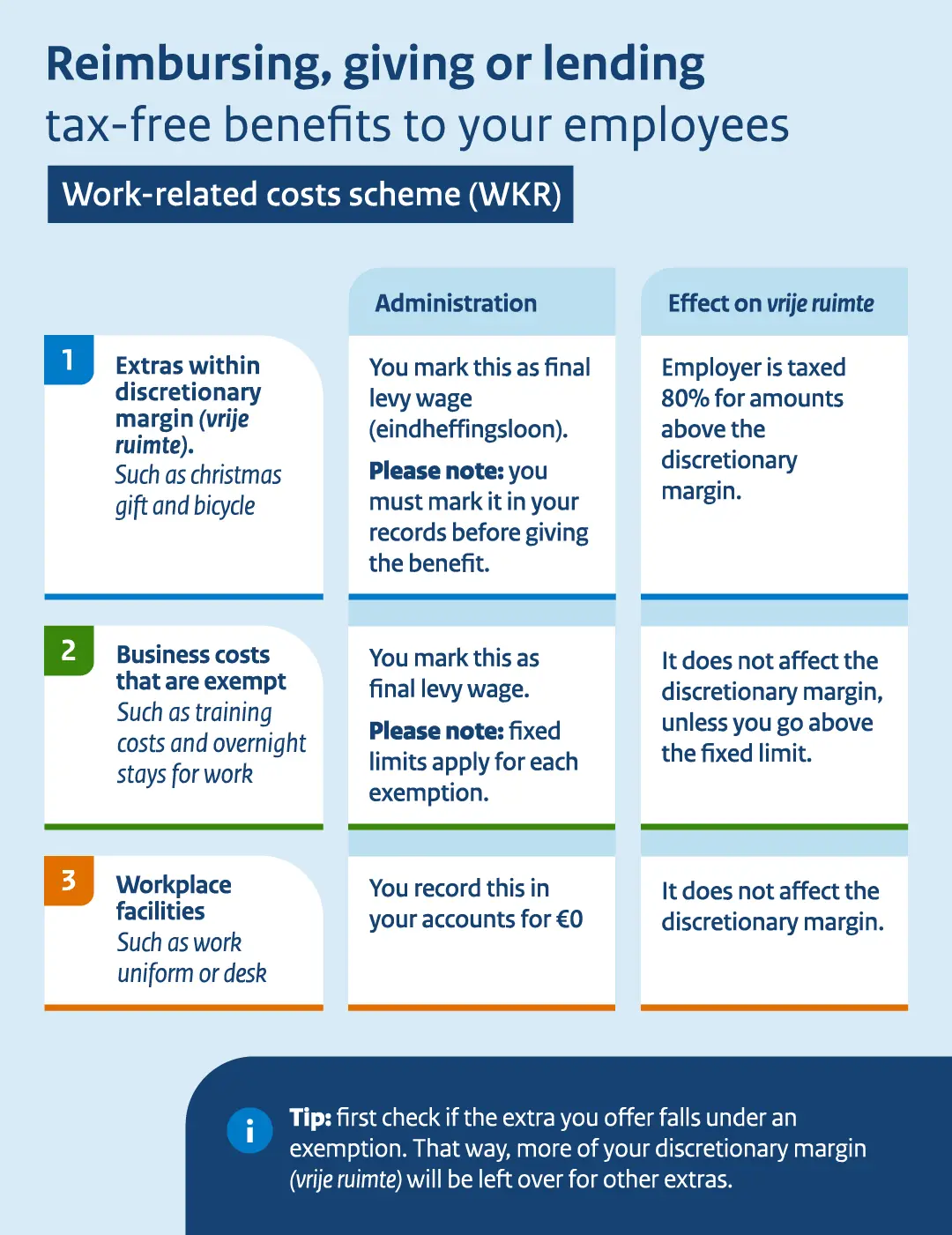

You can reimburse, give, or lend out extras.

Extras within discretionary margin

Examples:

- Sports membership

- Christmas gift

- Bicycle

Administration: you mark this in your administration as final levy wage. Please note: you must mark this before you give the benefit.

Effect on discretionary margin: employer is taxed 80% for amounts above the discretionary margin.

Exempted business costs

Examples:

- Travel costs

- Training costs

- Overnight stays for work

Administration: you mark these costs as final levy wage in your administration. Please note: fixed limits apply for each exemption.

Effect on discretionary margin: these costs do not affect the discretionary margin, unless you go above the fixed limit.

Workplace facilities

Examples:

- Desk

- Work uniform

- Coffee

Administration: you put this in your accounts for 0 € Effect on discretionary margin: these costs do not affect the discretionary margin.

Tip:

First check if the extra you offer falls under an exemption. That way, more of your discretionary margin will be left over for other extras.

What are the conditions for the WKR scheme?

If you want to use the work-related costs scheme, you must keep to the conditions:

- Stay within the maximum limit: as long as you remain within the discretionary margin (vrije ruimte), you do not have to pay wage tax on the value of the allowance. The discretionary margin is reassessed every year.

- Indicate the allowance in advance as final levy (eindheffing): This is income on which no tax needs to be paid. You can indicate this as ‘final-withholding wage’ in, for example, an email to your employee, in a staff handbook, or in the collective labour agreement (CAO). If you fail to do so, the Netherlands Tax Administration will treat it as ordinary income, and you will still have to pay tax on it.

- Do you spend more than the discretionary margin? Then you will pay tax on the extra amount (final levy). You do not have to pay national insurance contributions, employee insurance contributions, and employer's healthcare insurance contributions over this final levy amount.

You can learn more on how to calculate the discretionary margin and final levy in chapter 10 Vrije ruimte en eindheffing werkkostenregeling berekenen of the Dutch-language Payroll Taxes Handbook (pdf).

Specific exemptions and nil valuations

You can always reimburse certain expenses, provide benefits in kind, or make provisions for your employees without tax liability. You can do this through:

- specific exemptions (gerichte vrijstellingen): such as reimbursements for costs incurred by working from home, travel allowances, or costs incurred to pay for a certificate of conduct (VOG). Fixed rates apply per exemption.

- nil valuations (nihilwaarderingen): such as work clothing or refreshments at work.

You should first check whether a reimbursement falls into these categories. If it does, you can use the discretionary margin for other extras, such as a Christmas gift or another type of allowance. This will leave you with more discretionery margin.

You can find more information on specific exemptions and zero valuations in chapter 22 Gerichte vrijstellingen, nihilwaarderingen en normbedragen of the Dutch-language Payroll Taxes Handbook (pdf).

How to use the WKR scheme

As an employer you must justify the WKR when you file your payroll tax returns (aangifte loonheffingen). If you stay within the discretionary margin, you do not need to file and pay the final levy. Will you spend more than the discretionary margin? You will have to pay a final levy. You must justify the WKR in the second tax period of the following calendar year.